Spontaneous exchange of information

On 1 January 2017, the OECD/Council of Europe Convention on Mutual Administrative Assistance in Tax Matters (administrative assistance convention) entered into force for Switzerland. This makes provision for the obligation to provide spontaneous administrative assistance in Article 7. For the purposes of spontaneous administrative assistance, the convention will be applicable in Switzerland for tax periods from 1 January 2018.

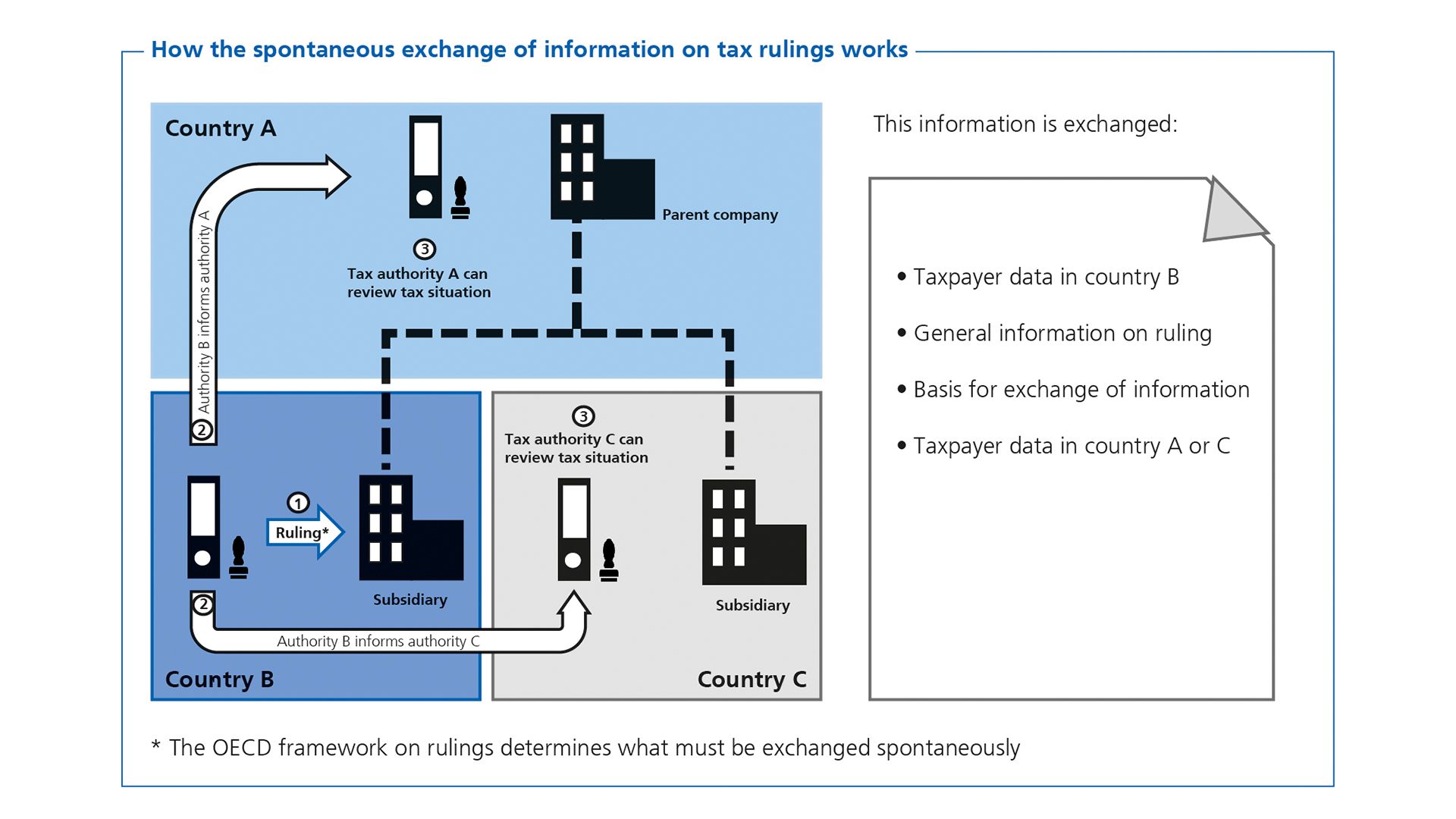

Information should then be exchanged spontaneously if the transmitting country suspects that the information available might be of interest to another country. In this context, spontaneous means that no request was submitted beforehand. As the initiative is always taken by the transmitting state, the spontaneous exchange of information has been handled very differently from country to country up to now.

Within the scope of the OECD and G20 project to combat base erosion and profit shifting (BEPS), the spontaneous exchange of information was specified for the first time in the area of advance tax rulings. These rulings are where there is a risk of base erosion or profit sharing. The Federal Council adopted the current international standard in this area in the context of a revision of the Tax Administrative Assistance Ordinance. Switzerland spontaneously exchanges information on advance tax rulings since 2018.